Quarterly results | NBFC

August 07, 2019

Shriram Transport Fin Co

BUY

CMP

1,000

Performance Highlights

Target Price

1,385

Particulars (` cr)

Q1FY20

Q4FY19

% chg (qoq)

Q1FY19

% chg (yoy)

Investment Period

12 Months

NII

1,962

1,906

2.9

1,823

7.6

Pre.Prov. Profit

1,543

1,512

2.0

1,406

9.7

Stock Info

PAT

634

746

(15)

573

10.7

Sector

NBFC

Source: Company, Angel Research

Market Cap (` cr)

22,286

For Q1FY2020, STFC has reported in-line numbers. For the quarter, PAT

Beta

1.4

increased 11% yoy, AUM growth continued to moderate at 6% yoy vs. 9% in

52 Week High / Low

1,450/903

Q4FY2019 and 22% in Q1FY2019. Key positive were stable asset quality with

Avg. Daily Volume

86,106

stage 3 at 8.5% and coverage +30% and credit cost for the quarter was 2.1%.

Face Value (`)

10

Management maintained credit cost guidance of 2% for FY2020.

BSE Sensex

36,690

AUM growth moderated; stable NIM: during the quarter, STFC reported AUM

Nifty

10,855

growth of 6% yoy, led by working capital (53% yoy on low base) and used vehicle

Reuters Code

SRTR.BO

loan (6% yoy). Used vehicle AUM led by M&CV segment grew at healthy rate of

Bloomberg Code

SHTF IN

15% yoy. Management guided for AUM growth of 15% yoy if growth improves in

2HFY2020 and increasing presence in rural area coupled with festive season,

which will support growth. NIM remained stable at 8.44% yoy (up 22bps qoq), as

Shareholding Pattern (%)

the company managed to pass incremental higher cost to borrowers.

Promoters

26.1

Asset quality steady; credit cost guidance maintained at 2%: Gross stage 3

MF / Banks / Indian Fls

8.1

increased marginally by 4%/declined 3% qoq /yoy. Provision for stage 3 declined

FII / NRIs / OCBs

56.4

by 259/222 bps qoq/yoy as it reversed additional provision made during Kerala

Indian Public / Others

9.4

flood. Management continued to guide credit cost for FY2020 at 2%.

Outlook & Valuation: We expect STFC’s AUM to grow at CAGR of 13% over

Abs.(%)

3m 1yr 3yr

FY2019-21E primarily owing to (1) post-election government to increase spending

Sensex

(1.1)

(2.6)

30.2

on infra project (macro recovery), and (2) pre-buying of CV before the BS VI will

SHTF

1.3

(29.5)

(22.4)

also improve the pricing of older vehicles. We expect STFC to report RoA/RoE to

2.7%/17.1% in FY2021E respectively. At CMP, the stock is trading at 1.2x

FY2021E ABV and 7x FY2021E EPS, which we believe is reasonable for

differentiated business model with return ratios. We recommend a BUY on the

stock with a Target Price of `1,385.

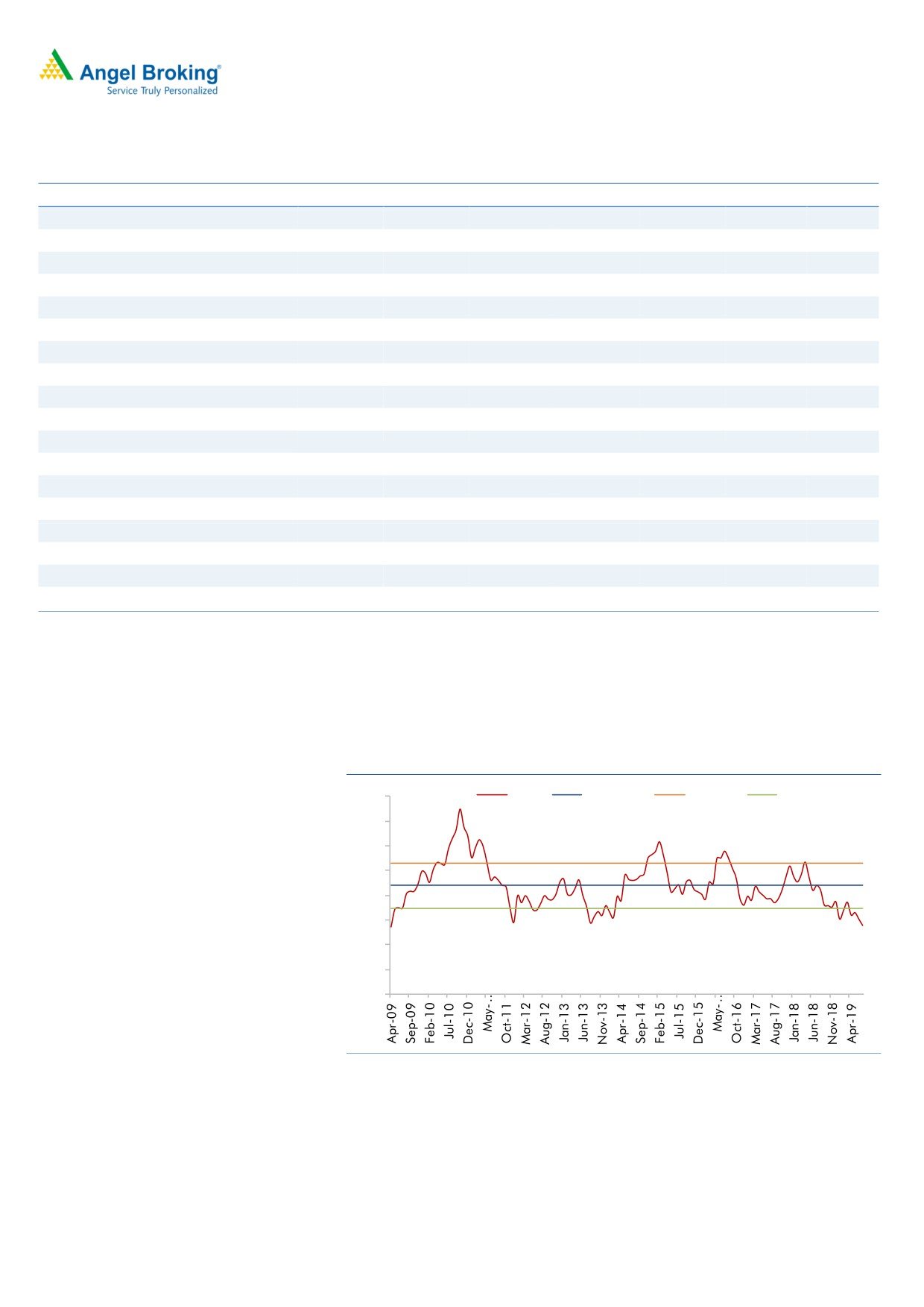

3 Year Price Chart

1800

Key Financials

1600

1400

Y/E March (` cr)

FY17

FY18

FY19

FY20E

FY21E

1200

NII

5,561

6,800

7,808

8,681

9,946

1000

YoY Growth (%)

10.1

22.3

14.8

11.2

14.6

800

PAT

1,257

2,460

2,562

2,868

3,405

YoY Growth (%)

6.7

95.7

4.2

11.9

18.7

EPS

55

108

113

126

150

Source: Company

Adj Book Value

425

504

607

697

815

P/E

18

9

9

8

7

P/Adj.BV

2.4

2.0

1.6

1.4

1.2

Jaikishan J Parmar

ROE (%)

11.7

19.8

17.4

16.7

17.1

Research Analyst

ROA (%)

1.8

2.9

2.5

2.6

2.7

022 39357600, Extn: 6810

Source: Company, Valuation done on closing price of 7/8/2019

Please refer to important disclosures at the end of this report

1